Guide to Taking Advantage of 0% Balance Transfer Offers

Based on requests from visitors, I have decided to compile my own guide to taking advantage of the credit card companies' 0% Balance Transfer Offers. I hope this guide will help everyone understand how to maximize the value of these offers and help boost your earnings for the year. If anyone has additional suggestions or tips - please post them in the comments.

What is a 0% Balance Transfer offer?

Most of us frequently get these annoying solicitation from credit card companies trying to get me to sign up for their credit card. Infact there are probably some in the advertising on this web site right now. Most of these offers include some gimmick or promotion to entice you to sign up for these offers.

A typical offer I see is "0% APR on Balance Transfers until 2007!" where the date given is typically 8-12 months in the future. Also, keep in mind the longer the balance transfer offer lasts the more you can make. I typically wait until I receive an offer that is at least 0% APR for 12 months. This is a 0% Balance Transfer offer - read on to find out how you can take advantage of them.

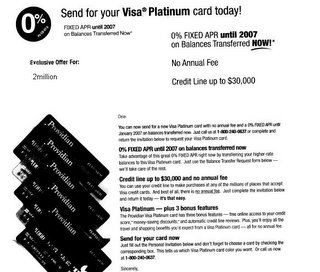

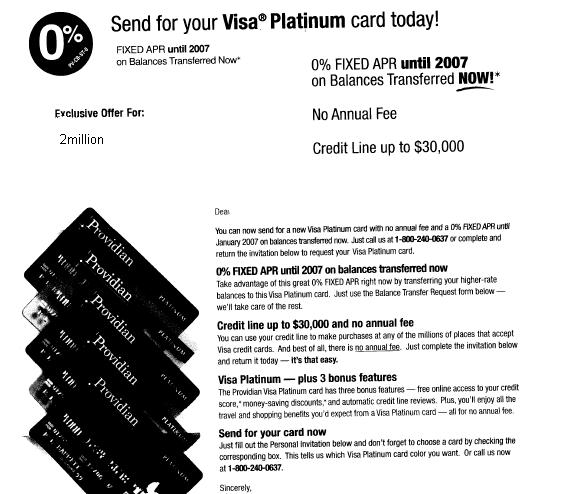

Here is an example of a credit card 0% Balance Transfer offer:

How do you screen out the less attractive offers?

Once you have a 0% Balance Transfer credit card offer, you need to review the fine print to make sure there are not any catches with the offer. The biggest catch out there in a small "balance transfer fee" typically 3% (but varies with each credit card company).

You want to make sure there are no balance transfer fees other fees associated with taking out a balance transfer. (Note: You can still profit if some of these fees are in the offer, but since these offers are frequent, I would just recommend waiting for a better offer).

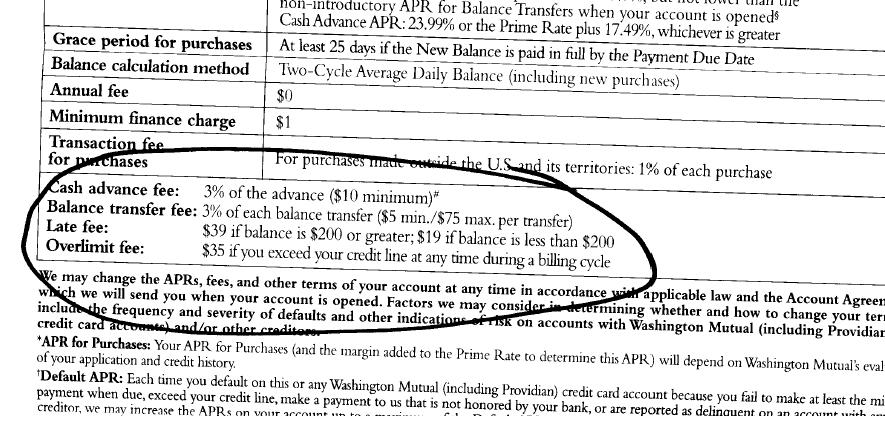

Here is an example of the fine print on balance transfer fees.

Notice this offer has a balance transfer fee of 3% ($5 minimum, $75 maximum). I prefer offers with no balance transfer fees at all, however if you can't find a no fee offer, one with a maximum may also work ok for you (just $75 less profitable in this example).

Now that I have an offer, how do I get access to this 0% balance transfer?

Fill out the application. I usually wait till I get the card in the mail so I know exactly what my limit is. When I call to activate the card, I begin the process of initiating a balance transfer. There are many techniques to choose from:

A) Ask for a check made out to you. I have done this for my Citibank credit cards. When you call to initiate a balance transfer I ask if I can get a check made out to myself. Its that simple. (Note: make sure you wont get a cash advance fee if you do this)

B) Apply the balance to other credit cards.

->B1) If you have a soon to be expiring 0% balance transfer then just ask that the balance transfer be used to pay off the balance on the old account.

->B2) Depending on how much you purchase every month on your credit cards, ask that the balance transfer be applied to you primary credit card to pay off your existing balance and any credit on you primary credit card account you can consume in future purchases. Instead of paying the balance on your primary credit card you spent, earmark those funds as your balance transfer funds.

->B3) If the first 2 options don't work, you can also consider having the balance transfer applied to a unused credit card account. When the transfer is complete you can call the credit card company and ask that a check for the positive balance be sent to you. (Note: I have heard from friends that some companies may not be willing to issue a check for the credit/positive balance so double check before trying)

C) If you have a HELOC have the balance transfer applied to this loan. Then you can write a check to yourself for the amount transferred.

D) If you have any type of loan, consider having the transfer amount paid to that loan. If you are planning on paying down/off the loan in the near future anyway you may be able to make a better rate of return by using the balance transfer to pay it off sooner rather than later.

I have used techniques A, B1, B2, and C all with great success to get access to the balance transfer loan.

Now that I have the 0% balance transfer, what do I do with it?

The whole reason you are doing this is to earn money, so this is a very important step. I always look for the highest-yielding risk free investment.

Here are some suggestions:

A) Online high yield savings accounts such as HSBC Direct, ING Direct, or EmigrantDirect.

B) If you have an outstanding balance on a HELOC or Line of Credit and you can pull back out money at anytime, consider paying down the HELOC or Line of Credit. You may make a better return on your money by saving on the interest payments.

C) Short term treasury bills on TreasuryDirect.gov.

D) Short term CDs such as a 6-month CD.

I have been putting my balance transfers in my EmigrantDirect and HELOC accounts.

How do I pay the balance transfer back?

Every month you should make the minimum payment on this credit card with the balance transfer. The minimum is usually somewhere around 2% of the balance. On a $10,000 balance transfer we are talking about a payment around $200 a month. I usually move the minimum payment amount from my savings account and try to pay the minimum payment as soon as I get the statement to avoid any risk of being late on my payment. To date, I have never been late with one of these payments.

I usually plan on paying back the entire balance of the balance transfer the month before the 0% APR expires. So if the offer expires in June 2006, I would pay the loan off in May to ensure I don't risk accumulating any interest on the loan. You can read the fine print of the credit card offer to determine exactly when the 0% APR expires and when the credit card company begins charging interest.

Other tips on 0% Balance Transfer offers

Taking advantage of these offers does lower your credit score. Its hard to tell how much, but I was surprised last year when my credit score fell significantly most likely due to taking advantage of several 0% offers. I currently have 2 0% balance transfer offers and my credit score appears to have recovered.

-Using balance transfers can help increase your liquidity. Having this "extra" cash in savings accounts with easy access to them, allows me to take my "emergency funds" and other short term savings and put them to work in more restrictive, but better return vehicles, like 1 yr bonds, or paying down some of my mortgage.

-Taking advantage of balance transfer offers can result in pretty significant returns. Last year I probably earned close to $700 in interest from money borrowed using 0% balance transfer offers.

-You typically cannot do a balance transfer from one credit card to another credit card offered by the same company.

-Read and re-read the fine print on the credit card. If you have questions call the credit card company and make sure they explain the fees to you.

Ready to give it a try?

You can start right now by checking out some of the advertisers on this web site. I bet there are a couple 0% Balance Transfer credit card offers on the right hand side of this web page.......

What is a 0% Balance Transfer offer?

Most of us frequently get these annoying solicitation from credit card companies trying to get me to sign up for their credit card. Infact there are probably some in the advertising on this web site right now. Most of these offers include some gimmick or promotion to entice you to sign up for these offers.

A typical offer I see is "0% APR on Balance Transfers until 2007!" where the date given is typically 8-12 months in the future. Also, keep in mind the longer the balance transfer offer lasts the more you can make. I typically wait until I receive an offer that is at least 0% APR for 12 months. This is a 0% Balance Transfer offer - read on to find out how you can take advantage of them.

Here is an example of a credit card 0% Balance Transfer offer:

How do you screen out the less attractive offers?

Once you have a 0% Balance Transfer credit card offer, you need to review the fine print to make sure there are not any catches with the offer. The biggest catch out there in a small "balance transfer fee" typically 3% (but varies with each credit card company).

You want to make sure there are no balance transfer fees other fees associated with taking out a balance transfer. (Note: You can still profit if some of these fees are in the offer, but since these offers are frequent, I would just recommend waiting for a better offer).

Here is an example of the fine print on balance transfer fees.

Notice this offer has a balance transfer fee of 3% ($5 minimum, $75 maximum). I prefer offers with no balance transfer fees at all, however if you can't find a no fee offer, one with a maximum may also work ok for you (just $75 less profitable in this example).

Now that I have an offer, how do I get access to this 0% balance transfer?

Fill out the application. I usually wait till I get the card in the mail so I know exactly what my limit is. When I call to activate the card, I begin the process of initiating a balance transfer. There are many techniques to choose from:

A) Ask for a check made out to you. I have done this for my Citibank credit cards. When you call to initiate a balance transfer I ask if I can get a check made out to myself. Its that simple. (Note: make sure you wont get a cash advance fee if you do this)

B) Apply the balance to other credit cards.

->B1) If you have a soon to be expiring 0% balance transfer then just ask that the balance transfer be used to pay off the balance on the old account.

->B2) Depending on how much you purchase every month on your credit cards, ask that the balance transfer be applied to you primary credit card to pay off your existing balance and any credit on you primary credit card account you can consume in future purchases. Instead of paying the balance on your primary credit card you spent, earmark those funds as your balance transfer funds.

->B3) If the first 2 options don't work, you can also consider having the balance transfer applied to a unused credit card account. When the transfer is complete you can call the credit card company and ask that a check for the positive balance be sent to you. (Note: I have heard from friends that some companies may not be willing to issue a check for the credit/positive balance so double check before trying)

C) If you have a HELOC have the balance transfer applied to this loan. Then you can write a check to yourself for the amount transferred.

D) If you have any type of loan, consider having the transfer amount paid to that loan. If you are planning on paying down/off the loan in the near future anyway you may be able to make a better rate of return by using the balance transfer to pay it off sooner rather than later.

I have used techniques A, B1, B2, and C all with great success to get access to the balance transfer loan.

Now that I have the 0% balance transfer, what do I do with it?

The whole reason you are doing this is to earn money, so this is a very important step. I always look for the highest-yielding risk free investment.

Here are some suggestions:

A) Online high yield savings accounts such as HSBC Direct, ING Direct, or EmigrantDirect.

B) If you have an outstanding balance on a HELOC or Line of Credit and you can pull back out money at anytime, consider paying down the HELOC or Line of Credit. You may make a better return on your money by saving on the interest payments.

C) Short term treasury bills on TreasuryDirect.gov.

D) Short term CDs such as a 6-month CD.

I have been putting my balance transfers in my EmigrantDirect and HELOC accounts.

How do I pay the balance transfer back?

Every month you should make the minimum payment on this credit card with the balance transfer. The minimum is usually somewhere around 2% of the balance. On a $10,000 balance transfer we are talking about a payment around $200 a month. I usually move the minimum payment amount from my savings account and try to pay the minimum payment as soon as I get the statement to avoid any risk of being late on my payment. To date, I have never been late with one of these payments.

I usually plan on paying back the entire balance of the balance transfer the month before the 0% APR expires. So if the offer expires in June 2006, I would pay the loan off in May to ensure I don't risk accumulating any interest on the loan. You can read the fine print of the credit card offer to determine exactly when the 0% APR expires and when the credit card company begins charging interest.

Other tips on 0% Balance Transfer offers

Taking advantage of these offers does lower your credit score. Its hard to tell how much, but I was surprised last year when my credit score fell significantly most likely due to taking advantage of several 0% offers. I currently have 2 0% balance transfer offers and my credit score appears to have recovered.

-Using balance transfers can help increase your liquidity. Having this "extra" cash in savings accounts with easy access to them, allows me to take my "emergency funds" and other short term savings and put them to work in more restrictive, but better return vehicles, like 1 yr bonds, or paying down some of my mortgage.

-Taking advantage of balance transfer offers can result in pretty significant returns. Last year I probably earned close to $700 in interest from money borrowed using 0% balance transfer offers.

-You typically cannot do a balance transfer from one credit card to another credit card offered by the same company.

-Read and re-read the fine print on the credit card. If you have questions call the credit card company and make sure they explain the fees to you.

Ready to give it a try?

You can start right now by checking out some of the advertisers on this web site. I bet there are a couple 0% Balance Transfer credit card offers on the right hand side of this web page.......

posted by 2million at

2/03/2006 07:23:00 AM

![]()

![]()

254 Comments:

2mill,

I plan on doing this in the near future after improving my credit score a little bit. I'm waiting for some things to fall off from the previous year as well as paying down my current 0% offer so that my utilization rate is lower. I've posted about exactly how much money you'd make with such an offer: 1st post and follow-up.

As I've noted in my second post, minimums are increasing to 4% and ED has increased their APY to 4.25%. If I transfer the money from ED directly to the CC every month, then I stand to make 3.32% APY.

Thanks for the post, very informative as usual.

By Frank, at 9:38 AM

Frank, at 9:38 AM

I've been following this topic pretty closely for some time now. Spent a lot of time on Fatwallet also. I started the process this week with interesting results. With a shotgun approach with apps this is what has transpired.

Citi Platinum Select - $3000

Citi Simplicity Rewards - Declined due to to many aps in 6 months

GM (HSBC) - Approved initially for $1500, asked to do a significant BT and got it bumped to $7000

Chase Cash Plus Rewards - $5000

Citi Professional - $6000

USAA - $25,000.

I wonder what USAA was looking at. Now it's time to fix the credit.

However, I've already hit my first hurtle. I applied for the highly recommended GM Card from HSBC. Initially, I was approved for $1,500. Not off to a great start. I called and explained that I wanted to do a balance transfer and picked an arbitrary number of $7,000. Underwriting approved it provided I tell them which cards to send the checks to. So, I actually have a balance of $3,500 on an MBNA and $1,200 on an AMEX. I asked they send $4,000 to MBNA and $2,000 to AMEX.

I was planning to pay off the balances from savings anyways. But I'm going to request MBNA and AMEX cut me a check for the overpayment. Putting all monies towards paying off the balances, then transfering the $6,800 into an equivalent ING acct.

I'm curious as to how other people would play out this situation. What do you recommend?

You also made a comment about paying off a HELOC. Have you factored in the "tax deduction" effect? How does the math play out on paying it off (or down) in addition to savings on payments, and interest deductions?

Thanks for your blog, huge help.

By Anonymous, at 10:41 AM

Anonymous, at 10:41 AM

Ryan,

I think I would try the same thing in regards to the GM balance transfer.

As far as the HELOC its actually (for me at least) comparable to putting the money in a savings account. For example say my fed/state inc tax rate is 33% and the HELOC and savings account were charging/paying the same rate.

With the HELOC I am losing a tax deduction of roughly 33% if I pay it off, but if I stuck the money in a savings account like EmigrantDriect, the interest I earned would be taxed at 33% so the after-tax rates in both cases would be the same.

By 2million, at 11:02 AM

2million, at 11:02 AM

Does anyone know how easy it is to significantly increase your credit limit on new cards? I just got my first 0% card for the purposes of this exercise and was given a $6800 limit (I stated my household income as 85G). When I activated the card I requested an increased limit to 10G which was granted within an hour.

Obviously the best way to take full advantage is to get as much money from each card, so I'm wondering if it's just a simple matter of requesting a higher credit limit after you get the card. As hungry as these CC companies are to give out balance transfers it seems like they would be willing to bump your limit 50% without problems. Anyone bump their limits as a matter of course?

By Anonymous, at 5:08 PM

Anonymous, at 5:08 PM

Have you ever tried making a balance transfer to your debit card? That seems like it would be an easy way of making a transfer. I am thinking of trying that.

Thoughts?

By Anonymous, at 10:23 PM

Anonymous, at 10:23 PM

For the little money you are making do you really think it is worth the cost of ruining your credit? I konw this would have to affect your credit somehow. Am I wrong?

By Anonymous, at 12:38 AM

Anonymous, at 12:38 AM

0% transfers are great! I do them about once every 2 years, and my credit score is well in the 750-800 range. One word of warning, like 2million said read and re-read the fine print! Read the big print too and keep the offers handy in case you ever need to refer back to them.

There are also 0% on NEW purchase offers, 0% on balance transfers, and 0% on both. Be wary!

I always just transfer over how much I have on my statement and then request a check. It's a great cash advance that doesn't get treated like a cash advance.

By Anonymous, at 2:06 AM

Anonymous, at 2:06 AM

I wonder if I could ever get a card like this since I never bought anything on credit (everything cash)

By Anonymous, at 2:50 AM

Anonymous, at 2:50 AM

I've noticed that my cards have all eliminated the max limit on cash advances recently, though the % still is 3%. This makes it more expensive to take out big cash advances and needs to be taken into consideration.

By Jojo, at 3:56 AM

Jojo, at 3:56 AM

This whole discussion is interesting but consider the following:

The risk of getting 'caught' unaware by the fine print on one of the credit card agreements, the lowering of your credit score due to opening up unsecured lines of credit (chasing these 0% deals), and the general behavior of living outside of your means (carrying around balances on credit cards in the first place) are worth examining.

For example, you transfer a balance to a 0% offer, it lowers your credit score, simply in the applying for a new card. You now go to borrow money for legit purposes (home, student loan), and due to your lower credit score, you are not given the best rates on 'real' debt. This debt is secured and typically longer in term. Where is the interest 'savings' now?

My advice is to spend the same amount of energy on adjusting your spending habits that you do on chasing the credit card deals. The 0% offers are the needles, and our overall culture of consumption as a lifestyle is the drug.

By Anonymous, at 9:02 AM

Anonymous, at 9:02 AM

Almost without exception, every blogger that advocates the 0% BT game notes the temporary negative impact that it will have on their credit score. If you're about to take out a loan, then this strategy is not for you. But there's a lot of us that simply don't care what our credit score is because we're not in the market for a loan.

Second, most of us are leaving the borrowed funds in an extremely liquid instrument like a high-yield savings account. If the CC company changes the promotional terms, then the funds can be returned within MINUTES via an online transaction.

Your advice is quite reasonable for the millions of people who misuse their lines of credit. But this strategy is geared toward those of us who are quite savvy when it comes to our finances. The bottom line is that 0% BT's are an extremely safe method of generating interest, provided you follow the rules in the fine print.

Crazy Money Blog

By Matthew, at 9:27 AM

Matthew, at 9:27 AM

Thanks for the post. I am currently planning on taking advantage of a similar offer on a credit card that I recently paid off with a credit limit of $23,700. With ING's promotional interest rates of 4.75% this is a great time to save money in those account.

I've used these balance transfers before and they will gladly wire them directly into your checking accout, which I find easier and quicker than having to write a check to myself.

By lpkitten, at 1:26 PM

lpkitten, at 1:26 PM

personnally, I prefer the fixed 1.9% "until paid off" offers better. You can take a decade (or more) to pay it back.

By Anonymous, at 1:26 PM

Anonymous, at 1:26 PM

personnally, I prefer the fixed 1.9% "until paid off" offers better. You can take a decade (or more) to pay it back.

The below story is based on personal experience with a Chase Visa card and which I have published elsewhere on a few forums in the past. It applies to this discussion if you take these loans to deposit elsewhere and still make charges on the same credit card.

--------------------------------------------------------------------------

Ever wonder why credit card companies constantly pitch you to consolidate your bills, take a vacation, improve the house, etc. using a cash advance loan at low teaser interest rates? There's a scam behind any offer you get from a credit card company, so beware. They aren't in the business of losing money.

These cash advance loans are always touted with low interest rates for some period of time (3.99%, 1.99% or even zero percent). Now, if you pay off all your charges on this account before you take out this loan and DON'T charge anything new until the cash advance loan is paid off, then you will be okay. But of course, most people don't do this.

And this is critical: what you may have missed buried in the fine print that I've seen with many credit cards is that if you have an outstanding balance when the cash advance is posted to your account or you make any new charges (in addition to this new loan amount), the payments that you subsequently make against the total owed will be FIRST allocated to the portion of your balance with the LOWEST interest rate.

Let's assume you regularly charge $400 monthly on this card and always pay the balance off with each monthly bill. So you never pay any interest to the credit card company. The credit card company is not happy about this, so they bombard you with checks with low interest rates for cash advance loans, hoping to entice you into a consolidation cash advance.

Now, due to some unplanned expense, you find you have to take a cash advance of $3200, perhaps offered at some very low annual interest rate (plus transaction fee), to cover that unexpected expense. And let's assume that you'll also keep charging your normal $400 monthly on this SAME card.

You'll now need to pay off $3200 extra (in addition to the regular $400 monthly) and you realize this will take you some months to do. Your intention is to keep making your regular payments to pay off your usual monthly bill and add something extra to pay down the cash advance loan over time. You don't think this will be too bad because, after all, you will only be paying 2% interest on the declining balance for the $3200 loan. So you increase your payments to $800 to cover the usual $400 monthly charges and then have the extra $400 applied to reducing the cash advance loan. Right? Wrong!

What the credit card company will do is allocate your full $800 payment towards the $3200 cash advance portion first because that portion of your balance has the lowest interest rate. Meanwhile they will charge you full interest (18% or whatever) on the $400 you charge each month (which becomes a growing balance continually exposed to the normal higher interest rates because it is not being paid down).

Result: You will pay a lot more interest than you thought by adding the loan at 2% interest and continuing to use the credit card.

While this method of allocating payments might seem logically backward to the consumer, it's a system that is very advantageous to the credit card company. Many people get drawn into deals like this and don't realize it until later on, if at all. And unless the government gets involved to protect the consumer from shenanigans like this, it isn't going to change anytime soon.

By Anonymous, at 11:11 PM

Anonymous, at 11:11 PM

Very good stuff.

As long as you are not applying for big credit in the near future, then it is alright.

Also, instead of opening up new CC, you can always just use the offers you get from your current cards, assuming that you have a zero balance.

By Bailey, at 10:36 AM

Bailey, at 10:36 AM

I have the 1.9% balance transfer. I'm required to purchase at least $25 per month on the card at 8.9%(which I do automatically). I borrowed 10K at 1.9% (which is waaay below the real inflation rate). ...seems $25/month at 8.9% per year is a reasonable price to pay for that loan? (at least until I get tired and decide to pay it off in full)

By Anonymous, at 2:24 PM

Anonymous, at 2:24 PM

Is there any way to get the CC company let you know your credit limit before filling in the application with the pre-approved offer?

I tryed several times. No result.

Thanks!

By Anonymous, at 8:30 PM

Anonymous, at 8:30 PM

I don't know why these credit card companies don't simply give us the interest we earn from their offer. Instead we have to go through this hassle of applying the damn credit card and put that money into a high yield savings account. Or is it because they have a math department on their side that have calculated the odds would be on their side that we would mess up with the new balance?

Now that I think about this. It would seem pretty scary if someone got your personal information and use it to make these balance transfer. I wonder if there's a way to prevent someone from opening up new credit cards using your personal information?

By Anonymous, at 1:44 PM

Anonymous, at 1:44 PM

Yes I have heard of a service that locks your credit and only lets credit accounts be openend on your credit when you authorize them - or something like that.

By 2million, at 7:36 PM

2million, at 7:36 PM

Dear $2M,

Am really enjoying your blog.

Also, I'd like to congratulate you on your accomplishments so far.

You really do stand far aheado of the pack in terms of net worth accomplishments. Don't rest on your laurels, but do realize you're doing something great.

I'm in my late 30s and also in N. Carolina. Married, with children, my situation is a bit different.

Not long ago we bought a house and I do remember the very significant difference in rates we would have paid each and EVERY year we keep our mortgage. We were pleasantly suprised when we learned our credit scores were about 40 points higher than we expected. That equates to about a $400 savings per year. A little more than 1/2 of the earnings one might achieve with the zero balance transfer (ZBT)game.

ZBT is just another approach to interest rate arbitrage, however, it's one that's complex and fairly risk prone.

Somehow I think that there are MANY other ways to earn $700. Perhaps a part time job, perhaps free lancing. I know there are many websites dedicated to free lancing for tech people. Actually, a part time 120 hour project would probably pay $6000 or more. Even after taxes it would be quite a bit more rewarding.

I agree with the early poster who recommended rechannelling your energy to finding ways to earn or save money rather than the ZBT approach. I whole heartedly agree.

Every time you open up a new card, you create new credit which diminishes the value of your credit line. Also, since the credit is maxed, that's a double negative.

Credit scoring formulas look for old, long established credit that's less than 50% utilized. The formulas are prejudiced against new credit as it may predict a pending financial crisis of the applicant.

I suppose if I did want to arbitrage interest rates I would like for some form of more easily understood cheap long term debt and a similar high return long term interest based investment. My gut says you'll only find something like that when borrowing against secured assets (like real estate) domestically and investing in foreign debt instruments (which introduce complexities like currency risk). Then again, several of the investment banking firms are offering mixed baskets of currencies in a pre-packaged mutual fund. The idea is that enough currencies (or foreign government bonds depending on the fund) will do well to offset the few that sink.

Well, at this point I'm rambling, so I'll wrap up with this thought.

At a certain time, maybe not to far from now, you'll have enough money to invest that spending time on ZBT rate arbitrage will not be woth the $700 you might make. Alternatively, additional investment in your career - which might be very time consuming - might also provide a superior reward.

Regards,

n

By makingourway, at 8:38 PM

makingourway, at 8:38 PM

When you pay (ex.1.9%) for a BT your ultimate profit is reduced further because you are paying with after-tax money.

I fully endorse the BT strategies though, and have been utilizing this process since the early 90s when banks would actually pay you up to 2% to use their money interest-free. At that time I maximized the system by completely paying off my fully mortgaged (9%) home in 5 years.

I currently have 9 BT offers and 1 HELOC (1.25%) totalling 250k in HSBC making 4.8%.

Just wanted to say that the system is definately not for everyone, but if you don't mind reading fine print and paying bills, it does work.

By Anonymous, at 10:35 AM

Anonymous, at 10:35 AM

Wow - $250k in oustanding BTs? Do you find it hurts your credit score significantly with so much outstanding?

Any additional suggestions to share?

By 2million, at 3:01 PM

2million, at 3:01 PM

Actually 100k is on the HELOC. I really do not keep a close eye on my credit score; it was 756 about 6 months ago. As far as the BT's, I have 16 credit cards and if I don't receive an offer in the mail, I don't hesitate to call and ask. I try to get BT's or promotional cash advances directly deposited to my HSBC account. I use Quicken to help keep track of deadline payments.

The best savings came about 3 years ago when I purchased another house with 8 credit card balances, all less than 5%. The savings came from not having to pay mortgage closing costs. After the house closing I immediately applied for a promotional HELOC with no closing costs.

One thing to watch-out for:My first promo % HELOC ran out so I paid the loan off and didn't realize I owed $100 for "no balance".OUCH!!

I need to invest in a nice magnifying glass.

By Anonymous, at 3:59 PM

Anonymous, at 3:59 PM

When you pay (ex.1.9%) for a BT your ultimate profit is reduced further because you are paying with after-tax money.

This is not total true. If you are careful with your accounting and keep your ZBT arbitrage card separate from your personal expenses, it's perfectly fine to deduct any interest or fees you pay as "investment expenses", just as you can deduct brokerage fees and trasaction costs.

By Anonymous, at 3:43 PM

Anonymous, at 3:43 PM

hi, I'm just trying to get my head around the 0% BT to reduce my HELOC debt for at least 12 months. Please correct me if I'm wrong in terminology... trying to convince myself I can deal with these CC companies -

I have $36,000 on my HELOC right now. I'm looking at getting the Discover Miles Card (it has good reviews) for its 0% APR (for both purchases and BT - its 0% if requested with acceptance form, also no BT fee) and 12,000 Discover Miles (worth $75).

If I can get a 20K credit limit, I'm thinking of BT 12K to the CC, to pay 1/3 of my 36K HELOC off. When I apply, would I ask for the BT to be "applied" to the HELOC?, or what's the correct term for this?

Months 1-11 - the intention is to make minimum payments (2-3%) to the CC, while maintaining the payments I have been making to my HELOC (minus the CC payments) - ie. to make a bigger dent into the HELOC payments.

Month 12 - pay the cc off with a check from my HELOC.

The net result should be good, right?? Look forward to your feedback!

By Anonymous, at 3:06 PM

Anonymous, at 3:06 PM

I have used business cash advances to consolidate my loans before, and now I'm wishing I would have waited, because this method of transferring to 0% credit cards would have been much more cost effective!

By Irene M., at 6:22 PM

Irene M., at 6:22 PM

People who want to save money from their credit card bills are now doing balance transfers of their debt from their existing credit card to a new credit card. Many credit card companies are offering attractive packages for balance transfers as a way of getting in more business.

0% balance transfers

By Parag, at 5:45 AM

Parag, at 5:45 AM

I completely consent with the article.

Советую проститутки Челябинска и проститутки СПб

By Проститутки, at 3:02 AM

Проститутки, at 3:02 AM

The post is pretty good.

Nokia Applications | Nokia Games | Nokia Themes | Nokia Prices | Nokia Reviews

By Junaid Ahmed, at 1:41 AM

Junaid Ahmed, at 1:41 AM

Its like you read my mind! You appear to know a lot about this, like you wrote the book in it or something. I think that you can do with some pics to drive the message home a little bit, but instead of that, this is great blog. A great read. I will definitely be back.

By διαγωνισμοι, at 1:18 AM

διαγωνισμοι, at 1:18 AM

The post is written in very a good manner and it contains much useful information for me.

By logo design competition, at 9:16 AM

logo design competition, at 9:16 AM

An excellent page you're having in here. Thanks for the share. Impressive page indeed..

By treatment for head lice, at 9:17 AM

treatment for head lice, at 9:17 AM

Very well done, excellent! This is what I need to know very much. Thanks for this informative post!

By baltimore hotel suites, at 1:44 AM

baltimore hotel suites, at 1:44 AM

I am very amazed with all the truths created here. I can boldly say that I can connect to this as well. I wish others would take the time to browse through this as well as I did.

commercial playground

daycare playground sets

daycare playground equipment

By ab.ghani, at 7:35 AM

ab.ghani, at 7:35 AM

That's really massive exposure post and I must admire you in this regard.

Affordable Web Design and Development

By Fabian Smith, at 6:08 AM

Fabian Smith, at 6:08 AM

Great post!

Cataratas en los ojos

By romancito2010, at 2:20 PM

romancito2010, at 2:20 PM

you’ve always shared with us. Just keep writing this kind of posts.The time which was wasted in traveling for tuition now it can be used for studies.Thanks

Aberdeen bed and breakfast

By Alex Mick, at 5:59 PM

Alex Mick, at 5:59 PM

Thanks for this article. It's just what I was searching for. I am always interested in this subject.

By Audio Logo, at 6:00 AM

Audio Logo, at 6:00 AM

Very useful you possess lots of understanding on this subject.

By Logo Design, at 5:33 AM

Logo Design, at 5:33 AM

Informative post.I am loving this information so much.Please keep such kind of the information in the future also.

By Make Facebook Timeline App, at 7:11 AM

Make Facebook Timeline App, at 7:11 AM

Many thanks for a lot of very good ideas. We anticipate reading through more on this issue in the foreseeable future. Keep up the great perform! This site will likely be wonderful useful resource and that i enjoy reading this.

By buy mortgage leads, at 10:06 AM

buy mortgage leads, at 10:06 AM

I really appreciate the blog since the first time do I saw it. Now they have reached another milestone which lead us to report about it.

By Logo Design Blog, at 2:03 AM

Logo Design Blog, at 2:03 AM

The article is clearly written and every point is factual and is no-nonsense. I have surf the internet looking for topics such as these and it is here where I find it written and stated well.

storage

By storage, at 8:37 AM

storage, at 8:37 AM

Its a brilliant writing. I hope Everyone like this writing. Thanks a lot for sharing this article.

By nmb bearing, at 8:54 AM

nmb bearing, at 8:54 AM

Nice Post. It’s really a very good.Community Logo Design I noticed all your important points. Thanks

By amhash, at 6:56 AM

amhash, at 6:56 AM

I am not in favor of credit card because when you purchase credit care then sale person talk in decent manner but when you not paying your credit card bill then they not respect you.

By Make Facebook Timeline App, at 5:33 AM

Make Facebook Timeline App, at 5:33 AM

There is certainly a great deal to know about this subject. I like all the points you have made.

By pearson taxi, at 6:13 AM

pearson taxi, at 6:13 AM

That is very good comment you shared.Thank you so much that for you shared those things with us.Im wishing you to carry on with ur achivments.All the best.

chat Mirc indir Sohbet Siteleri

By hayda, at 11:40 AM

hayda, at 11:40 AM

I am very impressed to read such a nice article, its contain very important and informative content that is highly appreciable. Good to visit here and I definitely visit here again in future. Beauty Reviews

By Unknown, at 8:27 AM

Unknown, at 8:27 AM

I read your post. That was amazing. Your thought processing is wonderful. Buy Gold Coins

By Unknown, at 2:11 PM

Unknown, at 2:11 PM

This comment has been removed by the author.

By Unknown, at 3:49 AM

Unknown, at 3:49 AM

Thank you for provided a good piece of information here so i can solve my credit card problem due to transfer zero balance online. Greg Mclardie

By Unknown, at 3:51 AM

Unknown, at 3:51 AM

Τhis is great blog. A great read. I will definitely be back.

By ofarmakopoiosmou, at 5:06 AM

ofarmakopoiosmou, at 5:06 AM

I like the blog. I believe this will be helpful in the future…

By Make iPhone App, at 6:09 AM

Make iPhone App, at 6:09 AM

This is great information for students. This article is very helpful i really like this blog thanks. I also have some information relevant for Dissertation Proofreading Services

By Unknown, at 7:35 AM

Unknown, at 7:35 AM

Great information you got here. I've been reading about this topic. I found it here in your blog. I had a great time reading this.

By App Marketing Online, at 8:13 AM

App Marketing Online, at 8:13 AM

This was a great and fun article for me to read. I have really enjoyed all of this very cool and fun information. This was really very interesting.

By Cheap Essay Writing, at 7:43 AM

Cheap Essay Writing, at 7:43 AM

Very informative and helpful. I was searching for this information but there are very limited resources. Thank you for providing this information…

By Cheap Essay Writing, at 11:16 AM

Cheap Essay Writing, at 11:16 AM

I really need to have or to share this all in one site.It has a total package that you are longing to look for great idea with it and very interesting details ..GOOD JOB for that!

By Branded Logos, at 6:32 AM

Branded Logos, at 6:32 AM

Thanks for sharing useful information.I am very much interested in reading articles. This blog was really an awesome site which I had never found it anywhere. Lots of stuff in this site ! Really helpful for most of them

By Photocopier Repairs Basildon, at 10:53 AM

Photocopier Repairs Basildon, at 10:53 AM

Hey it's really amazing. I like this trade show. Thanks for sharing this nice post.

By Cheap Essay Writing, at 1:16 PM

Cheap Essay Writing, at 1:16 PM

Excellent job done and nice informative blog posted. Paper Writing Services

By Paper Writing Services, at 1:57 PM

Paper Writing Services, at 1:57 PM

Brilliant! This is a really marvelous stuff for me. Must agree that you are one of the coolest blogger. I was curious to see a stuff like that. Fabulous post.

By Hire a PHP Developer, at 1:18 PM

Hire a PHP Developer, at 1:18 PM

Really great post, Thank you for sharing This knowledge.Excellently written article, if only all bloggers offered the same level of content as you, the internet would be a much better place. Please keep it up!

Hire PHP Developers Hire PHP Developers Hire PHP Developers

By Hire PHP Developers, at 1:55 PM

Hire PHP Developers, at 1:55 PM

Awesome post!!! Really enjoyed this post. But I want more information on such valuable topic .

By SEO Packages, at 12:56 PM

SEO Packages, at 12:56 PM

Thank you for posting the great content…I was looking for something like this…I found it quiet interesting, hopefully you will keep posting such blogs….Keep sharing

By Wholesale Towels, at 9:24 AM

Wholesale Towels, at 9:24 AM

Very significant article for us ,I think the representation of this article is actually superb one. This is my first visit to your site.

By Used Police Cars, at 9:41 AM

Used Police Cars, at 9:41 AM

I found so many interesting in your blog especially its discussion. keep up the good work.

By Debt Collection, at 7:43 AM

Debt Collection, at 7:43 AM

Thanks for the great post. Those who come to read your article will find lots of helpful and informative tips

By Hajj Packages, at 2:47 AM

Hajj Packages, at 2:47 AM

Nice article, thanks for sharing this information. Good to know that this topic is being covered also in this web site.

By Hajj Packages, at 3:40 AM

Hajj Packages, at 3:40 AM

The post is interesting. I really never thought I could have a good read by this time until I found out this site.Thanks.

By Debt Collector, at 4:14 AM

Debt Collector, at 4:14 AM

Your blog is very informative and gracefully, your guideline is very good.Thank you.

By Debt Collection, at 4:32 AM

Debt Collection, at 4:32 AM

This is so interesting blog. You are best listing knowledge provide at this site. I am very excited read this nice article. You can visit my site. Debt Collection

By Debt Collection, at 2:44 AM

Debt Collection, at 2:44 AM

I'm so glad I found this post because I've been looking for some information. Android App Marketing

By Android App Marketing, at 5:15 AM

Android App Marketing, at 5:15 AM

Thank you

By ครีมยางพารา, at 10:17 AM

ครีมยางพารา, at 10:17 AM

I did a little research on the topic and found that most people agree with your blog. Thanks.

By Anonymous, at 4:07 AM

Anonymous, at 4:07 AM

It’s really great article. I would like to appreciate your work and would like to tell to my friends.

By website designing company, at 4:28 AM

website designing company, at 4:28 AM

I like your website. Thank you for great information. I will come back to your website again.

best regards

By ครีมยางพารา, at 2:42 AM

ครีมยางพารา, at 2:42 AM

I appreciated on Author effort.who wrote the nice and informative post for us and also share with us. Custom Essays

By Custom Essays, at 2:40 PM

Custom Essays, at 2:40 PM

I think that this blog is really cool .so please visit my this site and get collection information. Dawn Travels

By Dawn Travels, at 8:47 AM

Dawn Travels, at 8:47 AM

Nice blog really good webpage and effort laid down suggestion are pretty good keep up the good work. Cheap Essay Writing

Cheap Essays

By Cheap Essays, at 2:35 PM

Cheap Essays, at 2:35 PM

Nice Post Love Reading Its

sbacterial infection

By Unknown, at 2:12 AM

Unknown, at 2:12 AM

I personally like your post; you have shared good insights and experiences. Its sounds exciting and it will really help me a great deal. Custom Essays

By Custom Essays, at 12:36 PM

Custom Essays, at 12:36 PM

plan on doing this in the near future after improving my credit score a little bit. I'm waiting for some things to fall off from the previous year as well as paying down my current 0% offer so that my utilization rate is lower.game dien thoai . Game bigone . tai bigone

By tai iwin, at 8:58 PM

tai iwin, at 8:58 PM

game iwin If I transfer the money from ED directly to the CC every month, then I stand to make 3.32% APY. game di dong .game avatar

By tai avatar, at 9:03 PM

tai avatar, at 9:03 PM

Very useful information

By KERDISETO, at 7:54 PM

KERDISETO, at 7:54 PM

thanks for post full of information.

I've always been tempted, but I'm not sure I have the "nads" to do it.

Perhaps the next card offer I get in the mail I'll check it out.

By unitysandvaseswedding, at 5:45 AM

unitysandvaseswedding, at 5:45 AM

wap auto game

By Unknown, at 9:55 PM

Unknown, at 9:55 PM

wap auto game

By Unknown, at 9:56 PM

Unknown, at 9:56 PM

Great, thanks for sharing this blog article.Really looking forward to read more. Fantastic.

By baju profesi anak, at 1:10 PM

baju profesi anak, at 1:10 PM

nice article keep blogging

Mauji

By Manoj Kusshwaha, at 2:45 PM

Manoj Kusshwaha, at 2:45 PM

nice article keep blogging

Mauji

By Manoj Kusshwaha, at 2:46 PM

Manoj Kusshwaha, at 2:46 PM

Awesome stuff. Thanks for sharing. I would like to bookmark this page.

By Coupon Missy, at 2:06 AM

Coupon Missy, at 2:06 AM

Awesome stuff. Thanks for sharing. I would like to bookmark this page. Coupon Missy

Coupon Codes

Free Shipping

Grocery Coupons

Aeropostale Coupons

ALDO Shoes Coupons

Amazon Coupons

American Eagle Coupons

Ann Taylor Coupons

AutoZone Coupons

Babies Online Coupons

Babies R Us Coupons

Banana Republic Coupons

Barnes and Noble Coupons

Barneys Warehouse Coupons

Beauty.com Coupons

Bebe Coupons

Bed Bath and Beyond Coupons

Best Buy Coupons

Beyond the Rack Coupons

BJs Wholesale Coupons

Bloomingdales Coupons

Bluefly Coupons

Build.com Coupons

Care.com Coupons

Columbia Coupons

Coupons.com Coupons

Diapers.com Coupons

Eddie Bauer Coupons

Express Coupons

Faucet.com Coupons

Gap Coupons

Groupon Coupons

By Coupon Missy, at 2:08 AM

Coupon Missy, at 2:08 AM

Very good information for future. Some informations are new. Really thank ful for the info.

web design company kottayam

By Anonymous, at 3:58 AM

Anonymous, at 3:58 AM

Very good stuff.

As long as you are not applying for big credit in the near future, then it is alright.

By Kursus SEO dan Internet Marketing Terbaik di Jakarta, at 6:24 AM

Kursus SEO dan Internet Marketing Terbaik di Jakarta, at 6:24 AM

just been reading this post and i have really enjoyed it. Thanks for providing a great service on this blog and i will be back for more!!!

Airport Taxi

By Airport Taxi, at 10:37 AM

Airport Taxi, at 10:37 AM

thanks for your article,like your blog very much,well done.

Airport Taxi

By Air Port Taxi, at 12:36 PM

Air Port Taxi, at 12:36 PM

what a post really nice thanks for the share.custom essays

By custom essays, at 2:16 AM

custom essays, at 2:16 AM

really informative and amazing post.

cheap essays

By cheap eassys, at 3:19 AM

cheap eassys, at 3:19 AM

helped alot. Thanx for the post. Keep up the good work !

By Airport Taxi, at 5:56 AM

Airport Taxi, at 5:56 AM

Very interesting and thanks for giving us this information.

By pasang iklan gratis tanpa registrasi, at 6:03 PM

pasang iklan gratis tanpa registrasi, at 6:03 PM

Wow amazing stuff I really enjoyed thanks for the amazing stuff.

Cheap Essays

By Unknown, at 2:27 AM

Unknown, at 2:27 AM

I konw this would have to affect your credit somehow. Am I wrong?

By On Hosting Domain, at 2:19 AM

On Hosting Domain, at 2:19 AM

Berikut ini adalah daftar backlink yang sangat cocok untuk anda yang sedang mengembangkan situs Download Lagu Terbaru :

http://musicmp3saya.blogspot.com/2014/07/musikgedecom-situs-download-lagu-terbaru.html

http://mp3-zone.mywapblog.com/download-lagu-terbaru-ya-di-musikgede-co.xhtml

http://musikgedeku.weebly.com/blog/situs-download-lagu-mp3-terbaru

http://musicmp3saya.blogspot.com/2014/08/musiksayacom-gudangnya-lagu-terbaru.html

http://infokomputer95.wordpress.com/2014/08/02/situs-download-lagu-musik-terbaru/

http://dekardi95.tumblr.com/post/93653430199/download-lagu-mp3-terbaru-2014-gratis

http://info-komputer.blog.co.uk/2014/08/02/download-lagu-terbaru-mp3-19032279/

http://dekardi95.livejournal.com/1665.html

http://musikgede.mywapblog.com/download-lagu-terbaru-gratis-dengan-muda.xhtml

http://ardigede394.blog.com/2014/08/03/download-kumpulan-lagu-mp3-terbaru-gratis/

http://gedeardi.blogdetik.com/2014/08/03/download-lagu-mp3-terbaru-di-sini/

http://downloadlaguterbaru.yolasite.com/

http://musikmp3kita.mywapblog.com/download-kumpulan-daftar-lagu-musik-mp3.xhtml

http://musikgede.webs.com/

http://www.musikgede.hol.es/2-uncategorised/2-download-lagu-mp3-terbaru-gratis

http://officialmusic38.wordpress.com/2014/08/06/download-gratis-lagu-mp3-full-album-terbaru/

http://dekardi95.tumblr.com/post/93936653664/download-lagu-barat-terbaru-gratis

http://musikgede.newsvine.com/_news/2014/08/06/25186501-download-kumpulan-album-lagu-terbaru-gratis

http://download-lagu-terbaru3.webnode.com/news/download-lagu-terbaru-lagu-korea-terbaru/

http://musikgede.jimdo.com/2014/08/06/download-kumpulan-lagu-india-terbaru/

https://sites.google.com/site/musikgedecom/

http://musikgede.besaba.com/?q=node/1

http://info-komputer.blog.co.uk/2014/08/10/download-lagu-terbaru-kumpulan-lagu-ost-mahadewa-antv-19091228/

http://ardigede394.blog.com/2014/08/10/download-kumpulan-lagu-jepang-terpopuler/

http://musikgede.jimdo.com/2014/08/11/download-kumpulan-lagu-korea-terbaru/

http://musikgede.blogdetik.com/2014/08/12/download-lagu-terbaru-kumpulan-ost-anime-jepang/

http://musikgede.newsvine.com/_news/2014/08/13/25328878-download-kumpulan-lagu-mp3-gratis-terbaru

http://dekardi95.tumblr.com/post/94610988074/kumpulan-link-download-tangga-lagu-terbaik

http://officialmusic38.wordpress.com/2014/08/13/download-kumpulan-lagu-indonesia-terpopuler/

http://musikgedeku.weebly.com/blog/download-kumpulan-lagu-bali-terbaru-gratis

http://www.doleta.gov/regions/reg05/Pages/exit.cfm?vexit=http://www.musikgede.com

http://www.prh.noaa.gov/cphc/jump.php?site=http://www.musikgede.com

http://www.samhsa.gov/samhsaNewsletter/redirect.aspx?url=http://www.musikgede.com

http://wwwcf.fhwa.dot.gov/exit.cfm?link=http://www.musikgede.com

http://www.onlinewebcheck.com/check.php?url=http://www.musikgede.com

By musiksaya.com, at 9:24 AM

musiksaya.com, at 9:24 AM

Financial Freedom is the best power site the next joys

By game lengkap terbaik, at 12:09 PM

game lengkap terbaik, at 12:09 PM

Pusat grosir SANDAL SANCU

By sancu jogja, at 12:15 AM

sancu jogja, at 12:15 AM

Very thoughtful. Definitely will share with my colleagues

By website designing india, at 5:25 AM

website designing india, at 5:25 AM

loved the way you discuss the topic great work thanks for the share...

By ASUS ZenFone Smartphone Android Terbaik, at 1:22 PM

ASUS ZenFone Smartphone Android Terbaik, at 1:22 PM

Have you ever tried making a balance transfer to your debit card? That seems like it would be an easy way of making a transfer. I am thinking of trying that.

Thoughts? :)

By My Feed, at 1:24 PM

My Feed, at 1:24 PM

nice post glad to be able to visit your blog and I really enjoyed the article on your blog

By Dunia Remaja, at 12:39 PM

Dunia Remaja, at 12:39 PM

I wonder what USAA was looking at. Now it's time to fix the credit.

:D

By Download Game Software Terbaru, at 4:26 AM

Download Game Software Terbaru, at 4:26 AM

think I would try the same thing in regards to the GM balance transfer.

As far as the HELOC its actually (for me at least) comparable to putting the money in a savings account. For example say my fed/state inc tax rate is 33% and the HELOC and savings account were charging/paying the same rate.

With the HELOC I am losing a tax deduction of roughly 33% if I pay it off, but if I stuck the money in a savings account like EmigrantDriect, the interest I earned would be taxed at 33% so the after-tax rates in both cases would be the same :D

By Download Free Mediafire PC Game, at 4:27 AM

Download Free Mediafire PC Game, at 4:27 AM

nice..tahnks for sharing

By baja ringan, at 2:54 AM

baja ringan, at 2:54 AM

nice info ..keep sharing

thanks

By baja ringan, at 11:06 PM

baja ringan, at 11:06 PM

Very nice formula and very useful to us.

Online Seo

By Unknown, at 2:55 AM

Unknown, at 2:55 AM

Thanks but I've always been tempted, but I'm not sure I have the "nads" to do it.

Citi Platinum Select - $3000

Citi Simplicity Rewards - Declined due to to many aps in 6 months

GM (HSBC) - Approved initially for $1500, asked to do a significant BT and got it bumped to $7000

Chase Cash Plus Rewards - $5000

Citi Professional - $6000

USAA - $25,000.

By NIX7, at 5:19 AM

NIX7, at 5:19 AM

thanks for share im really like this article

i cant wait for new article on this site

Blog Lupy Hakim

Lupy Hakim

Lowongan Kerja PT. Yamazaki Indonesia

Cara Melamar Kerja Lewat Email

By loker terbaru, at 3:23 AM

loker terbaru, at 3:23 AM

I think this is one of the most important information for me. And i am glad reading your article.

By Metland Rumah Idaman Investasi Masa Depan, at 8:08 AM

Metland Rumah Idaman Investasi Masa Depan, at 8:08 AM

With the HELOC I am losing a tax deduction of roughly 33% if I pay it off, but if I stuck the money in a savings account like EmigrantDriect, the interest I earned would be taxed at 33% so the after-tax rates in both cases would be the same :D

By hampton bay ceiling fans, at 9:43 PM

hampton bay ceiling fans, at 9:43 PM

Thanks for this article. It's just what I was searching for. I am always interested in this subject.

lowongan kerja mm2100 terbaru

By lowongan kerja mm2100 terbaru, at 2:00 AM

lowongan kerja mm2100 terbaru, at 2:00 AM

At least, we can belanja di elevenia gratis voucher 1 juta measure the total reputation in the development of oil technology through a series of racing activities that they do. Formula 1, WRC, Dakar to Le Mans endurance race is not the usual race. But in the event-the event Oli Motor Terbaik - Total Hi-Perf that, where performance and durability jasa seo so challenged, Total was able to prove the reputation of its technological advances. Sederat the trophy was already achieved.

By jasa seo, at 3:37 PM

jasa seo, at 3:37 PM

Soal Ujian Sekolah, Ujian Nasional dan Latihan Ulangan Harian Terlengkap di Indonesia - EduApps.co.id

Bisa dikatakan bahwa Bitcoin merupakan desentralisasi uang dan pindah ke pendekatan sistem yang sederhana internet telephony RCA Sparepart Motor Berkualitas Terbaik dengan Harga Terjangkau di Indonesia

yang oleh karena itu dapat digunakan sebagai bentuk 'uang swasta' dan dapat digunakan di kalangan 'kliring multilateral.

[Manfaat Yoghurt Bagi Kesehatan, Diet, Kecantikan dan Ibu Hamil] pada blog [On Hosting Domain] dalam jumlah yang jauh lebih kecil

(Rambut Sehat dan Bebas Botak) ..[REXCO Pelumas Anti Karat, WD-40 VS REXCO 50] sPara anggota kelompok didorong mengungkapkan pandangan mereka sendiri dan berbagi pendapat dengan anggota lain dalam kelompok yang sama., Pasal Sumber Disini

By Anonymous, at 3:58 PM

Anonymous, at 3:58 PM

Good work by the blog writer! such a nice and informative article keep sharing more articles. Cheap Essays

By Cheap Essays, at 2:45 AM

Cheap Essays, at 2:45 AM

This comment has been removed by the author.

By Unknown, at 1:43 AM

Unknown, at 1:43 AM

This comment has been removed by the author.

By Unknown, at 8:56 AM

Unknown, at 8:56 AM

Hi, free acne..

By Cara Menghilangkan Jerawat, at 11:27 AM

Cara Menghilangkan Jerawat, at 11:27 AM

I found this post to be very educational. Thank you for broadening my knowledge of this subject. No doubt its a great piece of writing as well. Thanks

By City Media Group, at 9:14 AM

City Media Group, at 9:14 AM

Thank you for sharing information. It is quite useful for us also. I always love to read such type of things.

doctoral dissertation

By kingwriters, at 5:54 PM

kingwriters, at 5:54 PM

This comment has been removed by the author.

By Unknown, at 10:43 PM

Unknown, at 10:43 PM

free

mp3

lagu

terbaru

top

top mp3

By Unknown, at 10:46 PM

Unknown, at 10:46 PM

unduh lagu

unduh musik

download music

stafaband mp3

stafaband video

download stafaband

muviza

bagishared

lagupedia

download lagu

download video

free download mp3

stafaband

stafaband 2017

lagu terbaru

download video youtube

downloader youtube

stafaband7

stafaband mp4

stafabands

download film terbaru

download lagu terbaru

4shared

bursamp3

bursalagu

wapkalagu

sharelagu

downloadlagugratis

savelagu

muvibee

azlagu

azlyric

gudanglagu

planetlagu

free download music and videos

By Info Pedia, at 2:56 PM

Info Pedia, at 2:56 PM

When it comes to beginning your own business, you certainly need better finance options and larger sums as well. In such cases, its best to consider business loans. OnDeck Small Business Loans

By Sandy Linter, at 1:46 AM

Sandy Linter, at 1:46 AM

Nice

web design company in chennai

web designing company in chennai

seo company in chennai

By Raga Designers, at 5:47 AM

Raga Designers, at 5:47 AM

Thank you for sharing such an excellent post.

"Creators Web India is Chennai No.1 leading Website Designers and Web Design Company in Chennai, India. Best services offer for Website Design & Development. We provide a Cost Effective and High Quality Ecommerce and CMS Websites. Looking for a professional Web Designer and Web Developer in Chennai? Start your Website Today!"

By creatorswebindia, at 7:18 AM

creatorswebindia, at 7:18 AM

Helpful post, thanks for sharing.

Blockchain certification

Blockchain course

Blockchain Training in Chennai

Blockchain Training near me

Blockchain course in Chennai

Blockchain Training Institutes in Chennai

By priya rajesh, at 4:28 AM

priya rajesh, at 4:28 AM

Thanks for sharing this information admin, it helps me to learn new things. Continue sharing more like this.

Angularjs Training in Chennai

Angularjs course in Chennai

AngularJS Training in Velachery

AWS course in Chennai

RPA courses in Chennai

DevOps Training in Chennai

By Sadhana Rathore, at 5:37 AM

Sadhana Rathore, at 5:37 AM

Great Article… I love to read your articles because your writing style is too good, its is very very helpful for all of us and I never get bored while reading your article because, they are becomes a more and more interesting from the starting lines until the end.

rpa training in chennai |best rpa training in chennai|

rpa training in bangalore | best rpa training in bangalore

rpa online training

By sakthi, at 12:52 AM

sakthi, at 12:52 AM

I believe that your blog would allow the readers with the information they have been searching for. Keep sharing more.

Spoken English Classes in Chennai

Spoken English Classes in Bangalore

English Speaking Classes in Mumbai

Spoken English Classes in Coimbatore

Spoken English Classes in JP Nagar

English Speaking Classes in Mulund

IELTS Classes in Chennai

By Anbarasan14, at 4:11 AM

Anbarasan14, at 4:11 AM

Great information!!! The way of conveying is good enough… Thanks for it

java course in madurai

java course in coimbatore

Best Java Training Institutes in Bangalore

Hadoop Training in Bangalore

Data Science Courses in Bangalore

CCNA Course in Madurai

Digital Marketing Training in Coimbatore

Digital Marketing Course in Coimbatore

By Riya Raj, at 1:29 AM

Riya Raj, at 1:29 AM

Excellent post thanks for sharing

Blockchain training institute in chennai

By jefrin, at 12:00 AM

jefrin, at 12:00 AM

Very impressive thanks for sharing

aws training in chennai

By jefrin, at 11:15 PM

jefrin, at 11:15 PM

Nice post thanks for sharing, i stay tuned!

By pharmanatura, at 3:08 AM

pharmanatura, at 3:08 AM

This is really a very good blog post and thanks for sharing it with the community!

By Web Design Company In Chennai, at 4:12 AM

Web Design Company In Chennai, at 4:12 AM

Nice blog post and thanks for sharing

web design company in chennai

website design company in chennai

web designing company in chennai

website designing company in chennai

seo company in chennai

By Raga Designers, at 1:43 AM

Raga Designers, at 1:43 AM

the article is nice.most of the important points are there.thankyou for sharing a good one.

UiPath Training Institutes in Chennai

rpa Training in Anna Nagar

rpa Training in T Nagar

By vijaykumar, at 5:18 AM

vijaykumar, at 5:18 AM

whatsapp group links 2019

By harish sharma, at 9:06 AM

harish sharma, at 9:06 AM

This comment has been removed by the author.

By Ram Niwas, at 1:06 AM

Ram Niwas, at 1:06 AM

Thanks for such a great article here. I was searching for something like this for quite a long time and at last, I’ve found it on your blog.thanks for sharing.

samsung service centres in chennai

samsung mobile service center in velachery

samsung mobile service center in porur

By vishwa, at 9:14 AM

vishwa, at 9:14 AM

Nice information. Thanks for sharing content and such nice information for me. I hope you will share some more content about. Please keep sharing!

Website Designing Company In Chennai

Best Web Design Company In Chennai

Web Design Services In Chennai

Web Design Company In Velachery

Website Development Company In Chennai

Web Development Services In Chennai

By sithararock, at 5:58 AM

sithararock, at 5:58 AM

Distributor Kuota

Indonesian Training Course

Service Center HP Indonesian

Service Center iPhone Indonesian

Service Center Acer Indonesian

PT Lampung Service

By Anonymous, at 2:29 AM

Anonymous, at 2:29 AM

Bài viết quá hay...

Bồn ngâm massage chân

Bồn ngâm chân

Có nên dùng bồn ngâm chân

Cách sử dụng bồn ngâm chân

By Chiến SEOCAM, at 6:13 AM

Chiến SEOCAM, at 6:13 AM

Before you update pls ad another pic to make it more looking good seo affiliate domination

Imjet set review

Jarvee review

By Anonymous, at 6:29 AM

Anonymous, at 6:29 AM

nice post...

Abacus Classes in chennai

vedic maths training chennai

abacus training classes in chennai

Low Cost Franchise Opportunities in chennai

education franchise opportunities

franchise opportunities in chennai

franchise opportunities chennai

Abacus institute Training Class in Chennai

Vedic Maths Classes in Chennai

Abacus Training Class in Chennai

By braincarve, at 3:46 AM

braincarve, at 3:46 AM

Nice information keep sharing with us.

web design company in Chennai

website designing company in Chennai

By RD Bytes, at 3:47 AM

RD Bytes, at 3:47 AM

technologytipsraja.com

IndiaYojna.in

ItechRaja.com

By technical raja, at 2:05 PM

technical raja, at 2:05 PM

very nice

Top 10 cars under 5 lakhs

Top 10 cars under 6 lakhs

top 5 light weight scooty

best suv under 10 lakhs

By saurav, at 6:43 AM

saurav, at 6:43 AM

1 bài viết quá hay và thú vị. Cảm ơn đã chia sẻ

lều xông hơi mini

mua lều xông hơi ở đâu

lều xông hơi gia đình

bán lều xông hơi

xông hơi hồng ngoại

By Chiến SEOCAM, at 4:08 AM

Chiến SEOCAM, at 4:08 AM

Thanks for Sharing Very Useful Article

infographic animation video services chennai india

ios app development chennai india

andriod application development chennai india

phone gap application development chennai india

iphone application development chennai india

By Massiveitsolutions, at 1:09 AM

Massiveitsolutions, at 1:09 AM

Thanks for Sharing

surgical operating microscope manufacturers in india

surgical operating microscope manufacturers

operating microscope manufacturers in india

ent surgical operating microscope manufacturers in india

By Sanma Medineers, at 1:12 AM

Sanma Medineers, at 1:12 AM

This comment has been removed by the author.

By Ram Niwas, at 8:04 AM

Ram Niwas, at 8:04 AM

Useful information

Top 5 best PPSSPP games for Android

Top 6 Best free online video convertor websites

Bill Gates admits losing to android as his biggest mistake

Top 9 best free tools and website to convert speech into text online

Advantages of choosing proper Antivirus for your PC

Top 8 Reasons Why Government Will Be Slow to Accept the Cloud

Things to be kept in mind while choosing a recovery software

Android vs. Other mobile Operating system and how google is best

Iamrjrahul WR3D 2K17

By Rahul, at 11:42 PM

Rahul, at 11:42 PM

free fire advance server

By Anonymous, at 1:53 AM

Anonymous, at 1:53 AM

lucky patcher

lucky patcher apk

luky patcher apk

lucky patcher download

download lucky patcher

lucky patcher for download

dowload lucky patcher

lucky patcher apk download

lucky patcher apk downlaod

download lucky patcher apk

luckypatcher apk download

lucky patcher apk downlod

download lucky pather apk

lucky pacher app

lucky patcher ap

lucky patcher apps

apps lucky patcher

lacky patcher app

apk lucky patcher

lucky patcher app download

download lucky patcher app

lucky patcher download app

download app lucky patcher

app cloner premium apk

lucky patcher games

game lucky patcher

games lucky patcher

lucky patcher game hack app

By SEO Web Agency, at 7:30 AM

SEO Web Agency, at 7:30 AM

Thanks for posting useful information.You have provided a nice article, Thank you very much for this one. And I hope this will be useful for many people.. and I am waiting for your next post keep on updating these kinds of knowledgeable things...Really it was an awesome article...very interesting to read..please sharing this information......I think your suggestion would be helpful for me. I will let you know if its work for me too. Thanks and keep post such an informative blogs.

By Askmetraveller, at 7:33 AM

Askmetraveller, at 7:33 AM

Thanks for sharing such a great information with us.Keep on updating us with these types of blogs.

professional web design company in chennai

top 10 web designing companies in chennai

By Unknown, at 5:17 AM

Unknown, at 5:17 AM

great content. really helpful

websitedesigners kerala

By Bitwissend Technologies, at 3:06 AM

Bitwissend Technologies, at 3:06 AM

This comment has been removed by the author.

By impressbss, at 6:47 AM

impressbss, at 6:47 AM

This comment has been removed by the author.

By impressbss, at 3:50 AM

impressbss, at 3:50 AM

This comment has been removed by the author.

By impressbss, at 7:57 AM

impressbss, at 7:57 AM

Thank you so much for your great informative information.

clipping path EU is offering all kinds of image editing services to the E-commerce Business Industries all over the world. It is offering clipping path service, Background Removal Service, Image Masking, Photo Retouching, Neck Joint Service, Color Correction and other related image editing service. The best thing is they are providing all their services in low cost. It is obvious that you are going to get satisfied.

By Clipping Path, at 7:36 AM

Clipping Path, at 7:36 AM

download call of duty mobile

download call of duty

download call of duty apk

call of duty mobile apk

battle ground call of duty

call of duty battle ground

Download COD Mobile Free For Android

download call of duty mobile Apk for Android

download call of duty mobile for IOS

download COD Mobile

call of duty game modes

download call of duty mobile lagends of war

download call of duty mobile lagends of war apk

download call of duty mobile

download call of duty mobile

download call of duty mobile

download call of duty mobile

download call of duty mobile

download call of duty mobile

call of duty mobile

By Mike, at 5:02 AM

Mike, at 5:02 AM

Hi there. Very cool site!! Guy ..Wonderful .. I will bookmark your website and take the feeds additionally…I am glad to locate so much useful info right here in the article. Thanks for sharing…

http://www.seputarpromojudi.com/

By Laurens99, at 1:41 AM

Laurens99, at 1:41 AM

A great read blog. Filorga very useful.

By Anonymous, at 3:35 AM

Anonymous, at 3:35 AM

Hanya dengan 1 user ID resmi para bettors sudah bisa bermain games yang ada di IDNlive ini, selain itu dalam hal bertransaksi di idnlive online ini juga sangat mudah dan tidak rumit.

By Laurens99, at 12:36 AM

Laurens99, at 12:36 AM

Pelayanan terbaik adalah prioritas utama dari Agen Judi idn poker Online. Kami menyediakan pelayanan customer service professional, sopan dan handal dalam bidangnya yang selalu siap membantu anda.

By Laurens99, at 6:18 AM

Laurens99, at 6:18 AM

thank you very much for share this wonderful article 토토사이트

By nowfirstviral, at 10:52 AM

nowfirstviral, at 10:52 AM

Web design company kerala

By Bitwissend Technologies, at 1:32 AM

Bitwissend Technologies, at 1:32 AM

I love your website your website is very good 파워볼사이트

By Great Viral, at 3:31 PM

Great Viral, at 3:31 PM

very nice article 토토사이트

By Viral, at 6:51 AM

Viral, at 6:51 AM

Top dance classes in Noida- indrayu

Dance classes in noida with the world's best dancers. Teach your children with our great dance teacher,

We provide dance classes for adults and kids,we are located in sector 50 noida

Our Dance teacher s having experience in every kind of dance style

You can also contact us for dance consultancy, we have won multiple medals and we also participate in different kind of dance programme, that’s why we are now top dance institute in noida 50, our success graph is going to above,

We also do dance workshop and function, our student already working in bollywood,

So if you are looking for

Top dance classes in Noida, zumba classes in Noida

also than you should contact Indrayu academy in noida

Address: Kothari International School B-279, Sector 50, Noida 201301

Phone: 0120 433 0844

By indrayu academy, at 4:18 AM

indrayu academy, at 4:18 AM

CCTV & Surveillance Solutions Dubai

We are best cctv installation services provider in Dubai

We provide service at your doorstep. If you need any kind of camera of cctv security issue, we will help you with that, we are certifiedcctv installation dubai company , our engineer is certified by dubai administration,

Our security expert can give you all details ,We also provide cctv if you need in bulk. We provide service in the office and for home also.

By Unknown, at 7:51 AM

Unknown, at 7:51 AM

A fascinating discussion is definitely worth comment. I do believe that you ought to write more on this topic, it might not be a taboo matter but generally people don't talk about such subjects. To the next! Cheers!!

Click here to getMoreinformation.

By greatrockdev, at 11:33 PM

greatrockdev, at 11:33 PM

Click here to tech cloud.

By hami, at 4:04 AM

hami, at 4:04 AM

thanks for your information.it's really nice blog thanks for it.keep blogging.

web design company in nagercoil

best web design company in nagercoil

website design company in nagercoil

web development company in nagercoil

website development company in nagercoil

web designing company in nagercoil

website designing company in nagercoil

digital marketing company in nagercoil

digital marketing service in nagercoil

web design company in nagercoil

best web design company in nagercoil

web design company in nagercoil

website design company in nagercoil

web development company in nagercoil

website development company in nagercoil

web designing company in nagercoil

website designing company in nagercoil

digital marketing company in nagercoil

digital marketing service in nagercoil

By thya, at 12:08 AM

thya, at 12:08 AM

Nice article.

Hello sport lovers. Enjoy these popular events from your home. I hope you'll enjoy these events.

47th Daytime Emmy Awards 2020 Live Stream

Saut Hermes 2020 Live Stream

World Junior Figure Skating Championships 2020 Updates

World Junior Figure Skating Championships 2020 Live

World Figure Skating Championships Live Stream 2020

Thanks.

By 47th Daytime Emmy Awards 2020 Live Stream, at 9:09 AM

47th Daytime Emmy Awards 2020 Live Stream, at 9:09 AM

Amazing blog thanks for sharing...

Web development company in Chennai

Web designing company in Erode

Software development company in Chennai

Digital Marketing Company in Chennai

By oceansoftware, at 2:10 AM

oceansoftware, at 2:10 AM

tata sky DTH company all details all problems

https://www.tataskycustomercare.com/

By celebratynews, at 12:44 AM

celebratynews, at 12:44 AM

Hey Nice Blog Post Please Check Out This Link for purchase

Men Satchel Briefcase Messenger Bags for your loved ones.

By Urban Dezire Official, at 8:35 PM

Urban Dezire Official, at 8:35 PM

Amazing article. It is very Helpful for me.

Watch cheltenham festival 2020 Live Stream

Thanks.

By StoneCold, at 9:33 AM

StoneCold, at 9:33 AM

Superb informational post.

Watch dubai world cup 2020 Live Stream

It helps us most. Wish you best of luck.

By StoneCold, at 9:40 AM

StoneCold, at 9:40 AM

You probably remember playing some fun video games as a child. Kids are now playing video games even more, and these games have become more advanced than ever. Therefore, video gaming popularity is probably not going to go down, so you should read the below article for some tips on how to utilize the video gaming experience 슬롯사이트.

By nowfirstviral, at 12:21 AM

nowfirstviral, at 12:21 AM

Superb Post. This helpful article is valuable to many. Check this article that may help many people in this fatal situation of COVID-19 attack. Please be safe with your family and friends.

CORONA VIRUS EFFECT ON SPORTING EVENTS

Thanks.

By StoneCold, at 9:30 AM

StoneCold, at 9:30 AM

Thanks for your informative article. This article is very informative for us. Thank You for this amazing knowledge 파워볼 메이저 사이트

By nowfirstviral, at 10:54 PM

nowfirstviral, at 10:54 PM

Very nice posts. this could not be explained better. Thanks for sharing, Keep up the good work 파워볼 메이저 사이트

By nowfirstviral, at 11:48 PM