Based on requests from visitors, I have decided to compile my own guide to taking advantage of the credit card companies' 0% Balance Transfer Offers. I hope this guide will help everyone understand how to maximize the value of these offers and help boost your earnings for the year. If anyone has additional suggestions or tips - please post them in the comments.

What is a 0% Balance Transfer offer?Most of us frequently get these annoying solicitation from credit card companies trying to get me to sign up for their credit card. Infact there are probably some in the advertising on this web site right now. Most of these offers include some gimmick or promotion to entice you to sign up for these offers.

A typical offer I see is "0% APR on Balance Transfers until 2007!" where the date given is typically 8-12 months in the future. Also, keep in mind the longer the balance transfer offer lasts the more you can make. I typically wait until I receive an offer that is at least 0% APR for 12 months. This is a 0% Balance Transfer offer - read on to find out how you can take advantage of them.

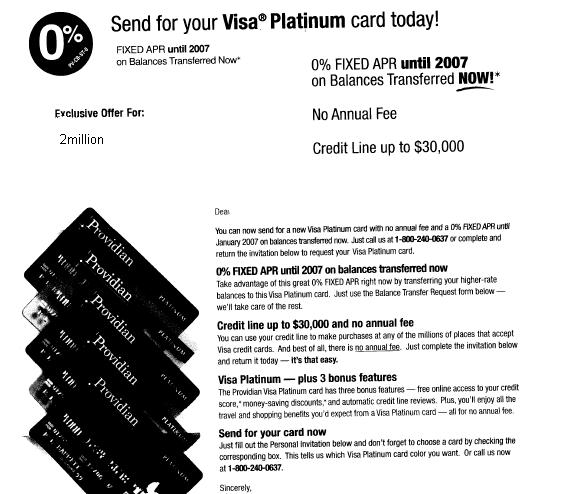

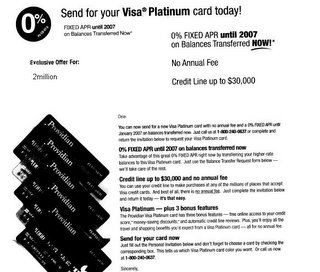

Here is an example of a credit card 0% Balance Transfer offer:

How do you screen out the less attractive offers?

How do you screen out the less attractive offers?Once you have a 0% Balance Transfer credit card offer, you need to review the fine print to make sure there are not any catches with the offer. The biggest catch out there in a small "balance transfer fee" typically 3% (but varies with each credit card company).

You want to make sure there are no balance transfer fees other fees associated with taking out a balance transfer. (Note: You can still profit if some of these fees are in the offer, but since these offers are frequent, I would just recommend waiting for a better offer).

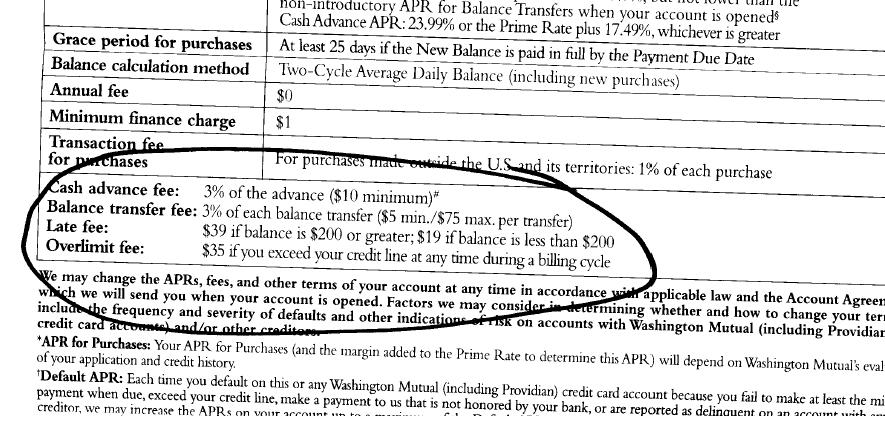

Here is an example of the fine print on balance transfer fees.

Notice this offer has a balance transfer fee of 3% ($5 minimum, $75 maximum). I prefer offers with no balance transfer fees at all, however if you can't find a no fee offer, one with a maximum may also work ok for you (just $75 less profitable in this example).

Now that I have an offer, how do I get access to this 0% balance transfer?Fill out the application. I usually wait till I get the card in the mail so I know exactly what my limit is. When I call to activate the card, I begin the process of initiating a balance transfer. There are many techniques to choose from:

A) Ask for a check made out to you. I have done this for my Citibank credit cards. When you call to initiate a balance transfer I ask if I can get a check made out to myself. Its that simple. (Note: make sure you wont get a cash advance fee if you do this)

B) Apply the balance to other credit cards.

->B1) If you have a soon to be expiring 0% balance transfer then just ask that the balance transfer be used to pay off the balance on the old account.

->B2) Depending on how much you purchase every month on your credit cards, ask that the balance transfer be applied to you primary credit card to pay off your existing balance and any credit on you primary credit card account you can consume in future purchases. Instead of paying the balance on your primary credit card you spent, earmark those funds as your balance transfer funds.

->B3) If the first 2 options don't work, you can also consider having the balance transfer applied to a unused credit card account. When the transfer is complete you can call the credit card company and ask that a check for the positive balance be sent to you. (Note: I have heard from friends that some companies may not be willing to issue a check for the credit/positive balance so double check before trying)

C) If you have a HELOC have the balance transfer applied to this loan. Then you can write a check to yourself for the amount transferred.

D) If you have any type of loan, consider having the transfer amount paid to that loan. If you are planning on paying down/off the loan in the near future anyway you may be able to make a better rate of return by using the balance transfer to pay it off sooner rather than later.

I have used techniques A, B1, B2, and C all with great success to get access to the balance transfer loan.

Now that I have the 0% balance transfer, what do I do with it?The whole reason you are doing this is to earn money, so this is a very important step. I always look for the highest-yielding risk free investment.

Here are some suggestions:

A) Online high yield savings accounts such as

HSBC Direct, ING Direct, or

EmigrantDirect.

B) If you have an outstanding balance on a HELOC or Line of Credit and you can pull back out money at anytime, consider paying down the HELOC or Line of Credit. You may make a better return on your money by saving on the interest payments.

C)

Short term treasury bills on TreasuryDirect.gov.

D) Short term CDs such as a 6-month CD.

I have been putting my balance transfers in my EmigrantDirect and HELOC accounts.

How do I pay the balance transfer back?Every month you should make the minimum payment on this credit card with the balance transfer. The minimum is usually somewhere around 2% of the balance. On a $10,000 balance transfer we are talking about a payment around $200 a month. I usually move the minimum payment amount from my savings account and try to pay the minimum payment as soon as I get the statement to avoid any risk of being late on my payment. To date, I have never been late with one of these payments.

I usually plan on paying back the entire balance of the balance transfer the month before the 0% APR expires. So if the offer expires in June 2006, I would pay the loan off in May to ensure I don't risk accumulating any interest on the loan. You can read the fine print of the credit card offer to determine exactly when the 0% APR expires and when the credit card company begins charging interest.

Other tips on 0% Balance Transfer offersTaking advantage of these offers does lower your credit score. Its hard to tell how much, but I was surprised last year when my

credit score fell significantly most likely due to taking advantage of several 0% offers. I currently have 2 0% balance transfer offers and my

credit score appears to have recovered.

-Using balance transfers can help increase your liquidity. Having this "extra" cash in savings accounts with easy access to them, allows me to take my "emergency funds" and other short term savings and put them to work in more restrictive, but better return vehicles, like 1 yr bonds, or paying down some of my mortgage.

-Taking advantage of balance transfer offers can result in pretty significant returns. Last year I probably earned close to

$700 in interest from money borrowed using 0% balance transfer offers.

-You typically cannot do a balance transfer from one credit card to another credit card offered by the same company.

-Read and re-read the fine print on the credit card. If you have questions call the credit card company and make sure they explain the fees to you.

Ready to give it a try? You can start right now by checking out some of the advertisers on this web site. I bet there are a couple 0% Balance Transfer credit card offers on the right hand side of this web page.......